Podcast: Play in new window | Obtain

When taking a look at common life insurance coverage–particularly within the context of its means to build up money worth–and evaluating it to different life insurance coverage merchandise like entire life insurance coverage, folks usually word that it seems to have a lot decrease ensures. The truth is, this is an excerpt from an listed common life insurance coverage proposal that highlights stated low assure: Now, let me provide you with some background on this coverage to be able to perceive a number of the amazement over this data.

Now, let me provide you with some background on this coverage to be able to perceive a number of the amazement over this data.

That is an listed common life insurance coverage coverage for a male age 45. It has a dying profit quantity of $815,241. In the event you’re questioning why the dying profit is such an odd quantity and never a neat spherical determine like $850,000 (for instance), it is as a result of this coverage was designed utilizing the deliberate premium quantity to calculate a essential dying profit (I will elaborate a bit extra on that in a bit). The deliberate premium for this coverage is $50,000 yearly (most likely sounds extraordinarily excessive if you happen to’ve all the time considered life insurance coverage as an expense, however there’s one thing else we’re capturing for on this case).

As a result of this coverage design makes use of a minimal Non-Modified Endowment Contract dying profit and can also be complies with the Guideline Premium Check, that $50,000 premium is the utmost allowable with out inflicting considerably unfavorable tax penalties to the coverage.

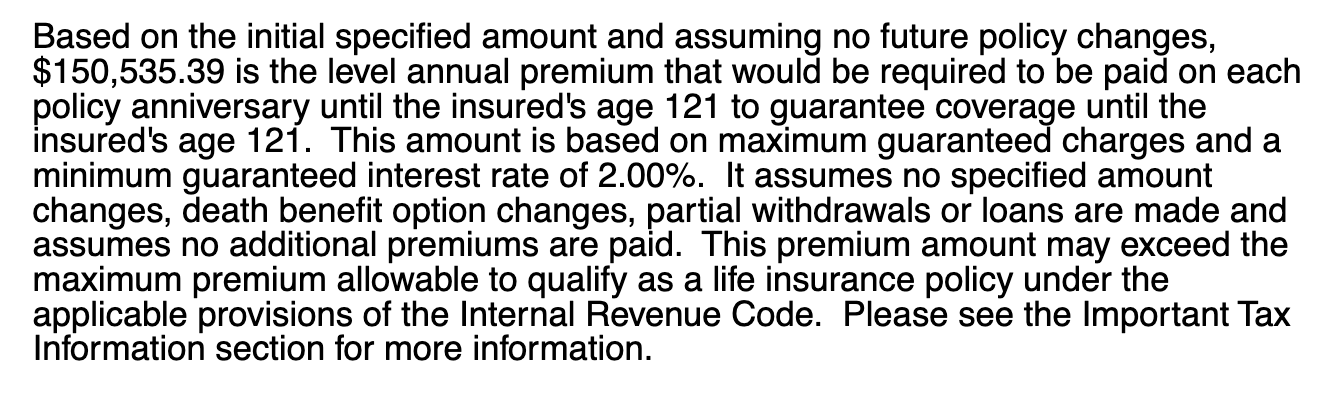

…however the quoted textual content, which was taken immediately from the company-issued proposal, clearly states that if the would-be coverage proprietor needs to assure that his preliminary $815,241 dying profit stay in pressure to his 121st birthday, he a lot pay a whopping $150,535.39. This sounds horrible.

And if he actually did want to assure his dying profit to his 121st birthday, this may be a fully horrible product selection. However that is not the objective right here so this truth is…moot for essentially the most half.

Totally different Life Insurance coverage Insurance policies Have Totally different Goals

There are lots of life insurance coverage insurance policies on the market. And this will likely come as a shock, however with all of this range of choices comes a range of aims tackled by completely different insurance policies.

Whereas many individuals understandably consider life insurance coverage as universally the identical–you pay a premium, and it pays a dying profit if you die–it isn’t. Some insurance policies search to supply a low-cost dying profit. Different insurance policies search to supply a excessive accumulation of money worth. Typically talking, these two aims are on opposing sides of a advantages spectrum.

If the person on this scenario wished to ensure an $815,241 dying profit to his age 121, there are merchandise that might do it for a lot lower than $50,000 per year-say nothing in regards to the $150,535.39.

But when, however, he desires to realize the best charge of return on a $50,000 annual cost right into a life insurance coverage coverage to construct wealth that enjoys many tax advantages, this product is arguably one of the best at the moment accessible available on the market.

Life Insurance coverage Ensures Price Cash

Life insurance coverage ensures price cash. That is true for each the insurance coverage firm and the coverage proprietor. The insurance coverage firm should shoulder the danger related to the dying assure and have ample reserves (i.e. cash it holds however may be very restricted in funding choices) to show it might make good on the assure. This price is mostly realized to the coverage proprietor via a lesser money worth accumulation on the coverage.

Insurance coverage firms are keenly conscious of this tradeoff, and produce merchandise to market that sacrifice ensures in favor of offering far more engaging non-guaranteed options–often expressed via money worth accumulation.

So in our instance above, the product in query has such a low assure relating to the dying profit as a result of it additionally has a particularly excessive potential to supply non-guaranteed money worth. The insurance coverage firm stripped excessive dying profit ensures from the product with the intention to afford the power to supply such greater money accumulating options.

The identical firm gives different common life insurance coverage merchandise. They’ve greater ensures. They may virtually positively accumulate a lot decrease quantities of money worth for a similar premium as our 45-year-old male insured.

![Life Insurance for a 30 year old woman [Top tips for best rates]](https://insuremonkey.com/wp-content/uploads/2023/04/Life-insurance-for-a-30-year-old-woman-350x250.jpg)

![Understanding AICPA Life Insurance Trust Refunds [Know Your Risks!]](https://insuremonkey.com/wp-content/uploads/2022/12/Understanding-AICPA-Life-Insurance-Trust-Refunds-120x86.png)

{kind=link}